As we move through the second quarter, we’re seeing trends that continue to align with the broader patterns anticipated for 2025. Interestingly, condominium inventory is up, signaling some renewed strength in that segment. In the single-family home market, monthly updates show that average list prices have increased, while average sale prices have declined—indicating that demand remains strongest around the median price point.

Land remains active, though it has yet to fully gain momentum this year, if it does at all. Meanwhile, the Farm & Ranch sector has some significant pending sales that may lead to strong closing volume later on, though activity remains slow for now.

One of the most notable observations this summer is a shift in buyer behavior. While not covered in the data here, external indicators suggest that online activity is high, but showings and direct inquiries are down. Buyers are spending more time researching from behind their screens and are more cautiously selective before engaging in person. Still, I see you—and I know you’re out there.

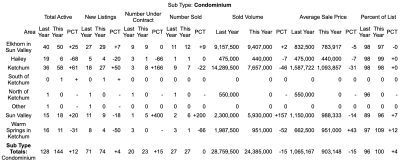

Condominiums

Inventory is up year-over-year, with a modest increase in new listings leading to a slight rise in pending sales compared to last year. However, total sales volume remains flat, and sold dollar volume is down — indicating a 15% drop in average sale price. Despite this, units are still closing at 100% of asking price on average, suggesting that listing prices have become more accurate and aligned with market expectations.

Ketchum and Elkhorn have both seen an increase in available inventory, particularly in Ketchum, where a surge of new units has contributed to increased activity. Elkhorn remains steady. Although Ketchum’s activity is up, average list prices are lower than they were a year ago, and sold volume is down 31%.

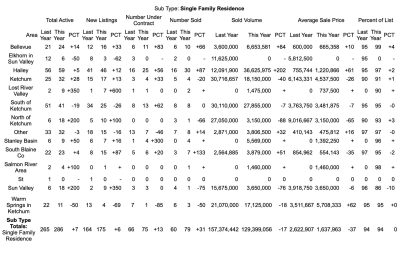

Single-Family Homes

In Q2 of 2025, single-family inventory increased across much of the valley — particularly in Ketchum and Sun Valley — while Hailey maintained strong, consistent numbers. In contrast, Elkhorn and Warm Springs saw reduced inventory. This likely contributed to a rise in Warm Springs’ average sales price, as the limited supply likely falls within higher price brackets.

The increase in inventory has correlated with an uptick in homes under contract, especially in areas like Bellevue and Hailey, which continue to perform well thanks to their more accessible, median price points. South Blaine County mirrors this trend.

Despite strong buyer demand, affordability differences across the valley have pushed the average sale price down 37%, resulting in a decline in total dollar volume. Ketchum, in particular, saw a 26% drop in average sales price due to fewer transactions.

The market remains dynamic, with varying strategies at play — especially in Ketchum, where competition is active and demand remains strong, though more calculated.

Lastly, it’s worth noting the relationship between list price and sale price: in the strongest market segments (Hailey, Bellevue, South Blaine), sale-to-list price ratios are highest. In less active or higher-end areas, that gap widens.

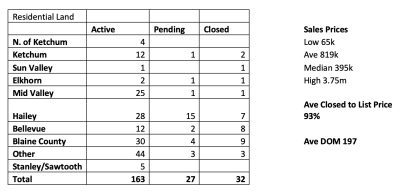

Land

Unfortunately, our MLS is currently experiencing glitches in compiling year-over-year data for land sales. In the meantime, I’ve done my best to reflect the present state of the market. At this point, land activity can be described as light—relatively underwhelming compared to the residential sector, and understandably so. Inventory is thinner, and construction costs remain high and variable.

That said, this sector tends to ebb and flow, with certain areas occasionally gaining momentum. Leading up to the 4th of July holiday, activity has been generally slow to gain traction this summer. Buyer behavior has become more cautious, and as we look toward 2025, it appears that land sales still haven’t found their stride—though that could shift as market dynamics evolve.

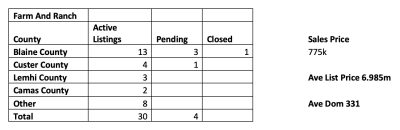

Farm and Ranch

Once again, due to MLS glitches, we’ve had to get creative in sourcing data that aligns with the residential market analysis. The Farm & Ranch sector is an exciting and unique niche to work in, but it spans a broader geographic area and functions on a different rhythm than other segments. Inventory is limited, days on market are typically high, and sales volume remains low. This segment isn’t expected to experience dramatic highs or lows—it tends to move steadily, with a handful of transactions here and there.