The 2025 market showed a clear shift toward balance and selectivity. While activity increased in some segments, pricing normalized after the highs of 2024. Buyers became more value-driven, and sellers who priced accurately continued to see success. Performance varied significantly by property type, reinforcing the importance of targeted strategy.

Condominiums

The condominium market strengthened in 2025, supported by increased transaction volume and higher overall sales dollars. Inventory rose modestly, while closed sales increased over 20%, indicating improved absorption. Although average sale prices dipped slightly, total sold volume climbed meaningfully, driven by higher-end units. Percent of list price softened marginally, reflecting healthy negotiation rather than distress.

Client Takeaway: Demand for lock-and-leave living remains strong. Well-located condos priced realistically continue to perform, while mid-tier inventory requires sharper pricing.

Single-Family Homes

Single-family homes remained the market’s primary driver, though conditions moderated from 2024. Inventory increased about 10%, and sales activity rose modestly. Total sold volume and average prices declined, signaling a normalization after peak pricing. Homes that were well-priced and move-in ready sold efficiently, while over-priced listings experienced longer market times.

Client Takeaway: This is a more balanced environment. Buyers have leverage, but quality homes still command strong interest.

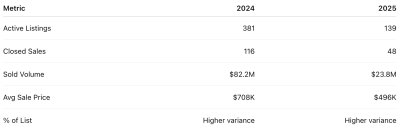

Residential Land

Residential land activity slowed notably in 2025. Inventory dropped sharply as fewer sellers entered the market, while closed sales and total volume declined. Buyers focused almost exclusively on parcels with clear access, utilities, and entitlement potential. Despite lower pricing, sellers who aligned with development realities achieved strong percent-of-list outcomes.

Client Takeaway: Land remains a long-term play. Build-ready parcels perform best; speculative land faces headwinds.

Farm & Ranch

The farm and ranch segment remained extremely thin. Inventory declined significantly, and sales were limited, reflecting long-term ownership patterns. Transactions that did occur were highly property-specific and driven by water rights, acreage, and lifestyle value rather than short-term market cycles.

Client Takeaway: Scarcity defines this segment. Opportunities are rare and relationship-driven.

As we move forward, expect continued normalization, selective buyer behavior, and strong performance for properties that are well-located, well-priced, and well-prepared. Strategy and positioning matter more than ever.