The Q3 2025 Blaine County Real Estate Market showed contrasting trends across property types. Condominiums led overall activity, driven by strong buyer demand in Ketchum and Sun Valley, while single-family homes remained steady with modest growth and near-full-price sales. In contrast, vacant residential land saw a sharp contraction, with minimal transactions and deep price reductions. The Farm and Ranch sector maintained exclusivity and value despite limited listings, as Idaho’s premium agricultural and recreational estates continued trading at or above list price. Collectively, Q3 2025 highlights a market defined by selectivity, premium pricing stability, and shifting buyer focus toward move-in-ready properties.

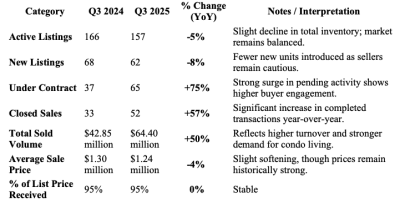

Condominiums dominated overall activity with 157 active listings (down 5%), but sold units surged 57% year-over-year. Ketchum led this growth, more than doubling sales (+110%) and tripling units under contract (+250%), pushing total sold volume up 120% to $39 million. Sun Valley followed with a 175% increase in sales and a 34% jump in sold volume. Elkhorn also improved, with +18% more sales despite a 12% dip in volume. In contrast, Hailey’s sales volume dropped 48%, and Warm Springs, though down 65% in listings, saw +50% in sales and +51% in volume. Average condo sale prices declined slightly overall ( –4% to $1.24 M), while list-to-sale ratios held steady at 95%.

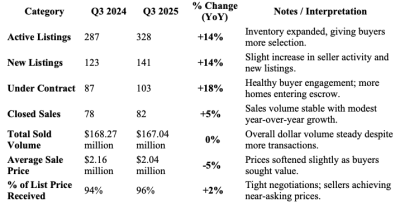

Single-Family Residences led the market, with active listings up 14% and sold units increasing 5% year-over-year. Total sales volume held essentially flat at $167 million, while the average sale price slipped 5% to $2.04 million. The strongest growth occurred in Ketchum, where sales surged 200% and total volume climbed 300% to $35 million, reflecting sustained demand for high-end properties. Sun Valley followed with sales up 50% and volume rising 29%. Lost River Valley and Stanley Basin also saw major growth, with sales up 300–400% and average prices soaring over 400%.

Conversely, Hailey and South of Ketchum, the county’s more accessible markets, experienced minor contraction—each seeing flat or negative sales volume around $27–47 million. North of Ketchum posted sharp declines, with sales volume dropping 87%.

The average list-to-sale ratio improved slightly to 96%, suggesting stable buyer-seller negotiation balance. Overall, the report highlights resilience in Blaine County’s higher-end submarkets while price-sensitive and peripheral regions continue adjusting to a slower pace of absorption

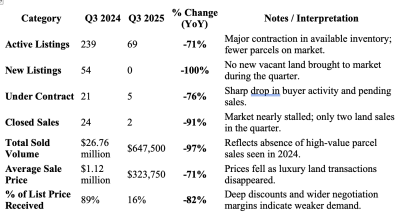

The Q3 2025 Vacant Residential Land Market across Blaine County and surrounding areas experienced a significant slowdown compared to 2024. Active listings fell 71% (239 to 69), with no new listings added and only two parcels sold—a 91% decline from last year’s 24. Total sold volume dropped 97% to $647,500, and the average sale price declined 71% to $323,750 as higher-end estate parcels disappeared from the market.

The list-to-sale ratio fell to 16%, reflecting wider negotiation margins and cautious buyer behavior. Most demand shifted toward developed properties, while many landowners withdrew or delayed listings. Sun Valley, Ketchum, and South Blaine County held the most inventory but recorded minimal activity, and outlying areas like Warm Springs and the Sawtooth Valley saw none.

Overall, Q3 2025 reveals a stagnant and highly selective land market, defined by minimal sales, downward pricing pressure, and buyers prioritizing clear value.

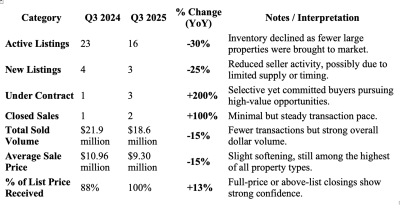

The Q3 2025 Farm & Ranch market in Idaho remains defined by low volume yet high-value transactions, underscoring its exclusive nature. Active listings dropped 30% (23 to 16), and new listings fell 25%, signaling limited turnover and cautious seller activity. Properties under contract rose 200%, indicating selective but serious buyer engagement. Closed sales held steady at two, matching last year’s minimal activity. Despite reduced volume, pricing remains near record levels with full-price or above-list closings common. Idaho’s agricultural and recreational estates continue to trade as rare, investment-grade assets, reflecting enduring demand within a highly selective, supply-constrained market.